Customs Information

Important information for sending parcels or pallets outside EU.

Customs documents

In addition, electronic customs data (EDI) must be submitted to customs for shipments, which contains information about the contents, value and recipient of the shipment. Customs clearance is primarily based on this electronic data. The commercial or proforma invoice serves as a supporting document for customs clearance and must contain the required information about the goods and the shipment. If necessary, the invoice can be attached to the shipment or submitted separately to support customs clearance. A copy of the invoice can be sent by email to address tullaus.fi@postnord.com and the original invoices can be attached to the shipment in a plastic pocket. Original invoices must be prepared in English and signed by hand if necessary (a signature is not required if the company is an authorized exporter for customs). Incomplete or incorrect customs data or invoice information may delay delivery or cause additional costs. For shipments to Norway, special attention must be paid to ensuring that customs information is transmitted electronically before the shipment arrives in the country.

Please note that there are areas inside EU that don't belong to the EU's tax territory. To these destinations you need commercial invoice or proforma invoice:

- Spain: the Canary Islands, Ceuta and Melilla

- Italy: San Marino and the Vatican

- Denmark: the Faroe Islands and Greenland (only postal shipments).

PostNord Parcel Locker and Service Point shipments to Norway

PostNord Parcel Locker and Service Point services can be used for shipments sent from the EU to Norway.

The commercial invoice must be addressed to one recipient (company) in Norway, who acts as the importer. This enables customs clearance of the shipment as a single entity (see consolidated shipment).

For shipments to Norway, it must also be ensured that the customs information is transmitted electronically (EDI) in the correct format before the shipment arrives in the country.

To ensure a smooth delivery, please contact our sales team well in advance of sending the first batch.

Shipments to Åland

Åland is part of the EU customs territory, but not the EU VAT territory.

Therefore, shipments between Åland and mainland Finland are treated as imports and exports for VAT purposes.

The declaration of import VAT for shipments crossing the Åland tax border has changed since the beginning of 2018.

You can find more information about shipments between Åland and mainland Finland on the Tax Administration website.

Shipments to the UK

Please note! Deliveries to the UK have been suspended for the time being. The reason for the suspension is the ever-changing import requirements of the UK's departure from the EU and the difficulties associated with them.

In addition to a commercial or pro forma invoice, an Importer Information form and a Direct Representation form are required for pallet shipments to the UK. The completed forms and a copy of the invoice must be sent by e-mail to our customs department at tullaus.fi@postnord.com.

Click here for instructions on shipping a pallet and filling out the Importer Information form.

Commercial invoice – for goods intended for sale

The commercial invoice is drawn up in English. If necessary, the invoice can be signed (a signature is not required if the company is an authorized exporter by customs).

The commercial invoice must include the following information:

• Exact address details of the sender and recipient, including contact persons

• EORI number

• Recipient's company number (“Registration number”) or identification details of a private individual

• Billing address

• Invoice number and date

• Tracking number or waybill number

• Delivery terms (e.g. DAP / DDP)

• Package contents / precise description of the goods using the usual trade name

• Weight (gross and net)

• Number of parcels or pallets

• Currency

• Customs heading (HS code) and possible export restrictions

• Country of origin

The information on the commercial invoice must correspond to the electronic customs data (EDI) transmitted to customs about the shipment.

Incomplete or incorrect information may delay customs clearance or cause additional costs.

Proforma invoice – gift or sample

You can use a proforma invoice instead of a commercial invoice when you do not charge the recipient for the goods.

The same requirements apply to a proforma invoice as to a commercial invoice. In addition, the invoice must state the reason why the goods are free of charge, for example, a sample, warranty repair or exhibition goods.

Please note that the invoice must always state the value of the goods (customs value), which cannot be zero. The value must correspond to the actual value of the goods from the point of view of customs.

The information on the proforma invoice must correspond to the electronic customs data (EDI) transmitted to customs from the shipment.

You can use our proforma invoice template.

Packing list – a document that specifies the item information of a shipment

A packing list is a useful, but not mandatory, document that specifies, for example, the number of items in a shipment, weight, volume, item numbers, and product-specific information such as colors and sizes.

A packing list supports customs clearance and receipt, but does not replace a commercial or proforma invoice or electronic customs data (EDI).

If necessary, a packing list can be attached to the shipment or delivered separately.

Split Shipment / Invoice (Split Shipment, Norway)

A split shipment means that several items are transported together and cleared as one entity with a single commercial or proforma invoice.

In a split shipment:

• customs clearance is made to one importer (company) in Norway, who acts as the party responsible for customs clearance of the shipment

• individual packages can be delivered to different recipients, but customs clearance is made to one party

The same information is required for a split invoice as for a commercial or proforma invoice. The invoice does not indicate individual delivery addresses, but the company receiving customs clearance in Norway.

A split shipment requires that:

• customs information is submitted electronically (EDI) as part of the shipping process

• the shipment is created and processed through the system used (e.g. TA system or integration)

• there is an importer in Norway responsible for customs clearance

A split shipment is particularly suitable for larger shipment volumes and requires separate implementation. Consolidation is not used for VOEC shipments.

To ensure a smooth implementation, please contact PostNord sales before starting your first shipments.

Letter of authorisation to export shipments to the Serbia and Bosnia-Herzegovina

For export shipments, the recipient is responsible for any import duties and taxes according to the delivery terms (e.g. DAP).

In some cases, the recipient country may require a letter of authorisation (Power of Attorney) from the recipient, which ensures that the recipient is responsible for customs clearance of the shipment and related fees.

The need for a Power of Attorney depends on local customs requirements and the recipient's situation.

The sender can ensure a smooth delivery by asking the recipient to fill out a Power of Attorney in advance if necessary.

Letter of authorisation for a recipient in Serbia or Bosnia-Herzegovina

EUR.1 movement certificate (certificate of origin)

The origin of the goods can be proven by an EUR.1 movement certificate or an exporter's declaration (commercial invoice declaration).

The EUR.1 movement certificate is used when it is desired to benefit from a customs advantage based on free trade agreements (e.g. reduced or zero customs duty in the country of destination).

The EUR.1 certificate is applied for from the customs authority at the place of export customs clearance, and if necessary, it must be validated by customs. The exporter fills in the application part of the certificate and submits it to customs for validation.

Alternatively, the exporter can in certain cases use a commercial invoice declaration (exporter's declaration), if the conditions are met (e.g. approved exporter or based on the value of the shipment).

The certificate of origin is used in the country of destination to obtain a customs advantage.

Please note that the EUR.1 certificate is not a mandatory document, but is only used if the customs advantage is desired.

Exporter declaration (commercial invoice declaration)

An exporter's declaration (commercial invoice declaration) is an alternative way to prove the origin of goods.

Every exporter has the right to draw up a commercial invoice declaration for an originating product if the value of the consignment does not exceed EUR 6,000.

An authorised exporter can draw up commercial invoice declarations regardless of the value of the consignment. A company that regularly exports originating products can apply to become an authorised exporter.

In some cases, the REX system (registered exporter) can also be used to prove origin.

An exporter's declaration is used when one wishes to benefit from a tariff preference based on free trade agreements in the country of destination.

Please note that an exporter's declaration is not a mandatory document, but is only used if one wishes to benefit from a tariff preference.

*EORI number

The EORI number (Economic Operators Registration and Identification) is a company customs number that is issued by the customs authority of a member state to companies operating in the EU.

When registering in one EU country, a company receives an EORI number, which is used in all EU countries in connection with customs clearance.

The EORI number is needed when a company acts as an exporter or importer and makes customs clearances.

In Finland, the EORI number consists of the company's Business ID in the format FI1234567-8.

You can apply for an EORI number from Finnish Customs.

When exporting to Norway, the EORI number is used as part of the export customs clearance process.

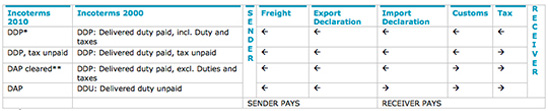

Incoterms – terms of delivery

The Incoterms 2020 delivery terms define the responsibilities of the seller and the buyer for delivery, goods and costs.

When exporting outside the EU, the commercial invoice must state the delivery term used and the place of delivery (e.g. DAP, Street 1, NO-0123 Oslo).

The delivery term determines in particular who is responsible for import-related costs and customs clearance in the country of destination.

The most common delivery terms are:

DAP (Delivered At Place) – the recipient is responsible for import customs clearance, VAT and other charges in the country of destination

DDP (Delivered Duty Paid) – the sender is responsible for customs clearance and related costs

In PostNord services, the delivery term may vary depending on the service. For example, MyPack Collect and [SE4.1]PostNord Pallet are generally delivered according to the DAP delivery term.

Please note that the delivery term directly affects who pays the import costs of the shipment, especially for shipments to Norway.

*! Note: The DAP delivery chain clauses must state the place of delivery, e.g. DAP, Street 1, CH-1234 Zürich.

For customs purposes, "import" means bringing goods to Finland from a country outside the EU. The goods must be cleared before they can be used or resold. The most common customs import clearance method is the release of goods for free circulation and consumption. This method requires a customs declaration.

Import shipments to Finland

In customs operations, import refers to the bringing of goods into Finland from a country outside the EU.

The goods must be cleared through customs before they can be put into use or sold on.

The most common customs procedure for import is release for free circulation and consumption. In this procedure, a customs declaration must be submitted to the customs authority for the goods.

The customs declaration is in practice submitted electronically, and any customs duties and VAT are determined on the basis of this declaration.

Taxes and payments

The taxes and fees to be levied are determined based on the customs heading (HS code), origin and customs value of the goods.

The most common taxes levied upon import are customs duty and value added tax. Customs duties may be levied on goods imported from third countries unless free trade agreements, tariff quotas or tariff suspensions reduce or eliminate the customs duty.

As of the beginning of 2018, the VAT on imports has been transferred from Customs to the Tax Administration. Companies liable for VAT declare the VAT on imports in their own tax return.

Customs issues a decision in connection with customs clearance stating the customs value and any duty collected. The VAT on imports is calculated and reported separately to the Tax Administration.

Please note that for international shipments (e.g. to Norway), the payer of taxes and fees is determined by the delivery terms (Incoterms) or the customs clearance model used (e.g. VOEC).

VOEC (Norwegian VAT on E-Commerce)

VOEC (VAT On E Commerce) is the Norwegian VAT system used for e-commerce shipments sent to consumers (B2C).

In the VOEC system, VAT is already paid in connection with the purchase transaction in an online store. In this case, the recipient in Norway does not incur separate customs clearance or VAT costs in connection with the delivery.

The VOEC system can be used when:

• the shipment is to a consumer (B2C)

• the value of an individual product is no more than 3,000 NOK

• the shipment does not contain restricted or excise goods

For VOEC shipments, you must:

• add the VOEC number to the shipment's customs data (EDI)

• declare the value of the goods excluding VAT

• provide product-specific information (e.g. description and value)

If the VOEC conditions are not met, the shipment will be cleared as a normal import and the recipient will pay VAT and any customs costs in Norway.

For more information about VOEC shipments and implementation, please contact PostNord sales.

Shipping options to Norway

When shipping to Norway, it is important to choose the right customs clearance model depending on the type of shipment.

The most common options are:

• VOEC – consumer shipments (B2C), where VAT is paid at the purchase stage

• Normal import (DAP / DDP) – shipments where the recipient or sender pays customs clearance and taxes

• Split Shipment – combining several items into one customs clearance

Choosing the right model affects, among other things, delivery times, costs and the recipient's experience.

For more information on choosing the right solution, contact PostNord sales.

The most common mistakes in customs clearance

The following deficiencies may delay the shipment or cause additional costs:

• incomplete or incorrect customs data (EDI)

• overly general description of goods (e.g. "goods")

• declaring the value of the goods incorrectly (e.g. €0)

• VOEC number is missing or not in the customs data

• wrong delivery terms (Incoterms)

Make sure that the shipment information is correct both on the invoice and in the electronic customs data.

What the sender must ensure

Before sending the shipment, please ensure that:

• the goods have the correct description and value

• the commercial or proforma invoice has been correctly completed

• the customs information (EDI) has been correctly submitted

• the delivery terms (Incoterms) used have been specified

• the necessary additional information (e.g. VOEC number) has been added

Incomplete information may lead to delays in customs clearance.

Further information

Further information is available on the Finnish Customs' website www.tulli.fi.

PostNord customer service will also help you:

email: tullaus.fi@postnord.com